XVA calculations have become an important part of quantifying long-term risks in commodities, but they can be computationally challenging and expensive. Many vendor solutions lack standardization and transparency, while in-house solutions may struggle to keep up with functionality and performance requirements. As a result, organizations too often rely on internal built or black box 3rd party on premise solutions that just approximate the necessary calculations and introduce additional vulnerabilities. Our commodities trading clients are using Beacon Platform to address these issues, delivering better and faster XVA reports that enhance risk management of complex commodity derivatives.

Providing transparency and extensibility

As part of Beacon’s overall risk reporting framework and commodity portfolio management, XVA can be run on any desired selection of trades, books, portfolios, and counterparties, and natively handles trade lifecycles. Calculations for XVA are fully visible in the platform, thanks to Beacon’s transparent source code. Customers can view the underlying logic, question what the models are doing, and better understand what the resulting numbers mean. Calculations are readily extensible across new markets and instrument types as they are added. Clients can create XVA metrics starting from the actual state of the market or from an adjusted level for evaluating different scenarios.

Beacon’s XVA uses a best-in-class “Future Exposure” approach, involving simulation of all relevant commodity market rates and prices and full revaluation and evolution of trades to maturity. It models a counterparty’s ISDAs and CSAs to simulate future collateral postings and computes a range of XVA metrics. Calculations for these reports are run in Beacon’s cloud-native elastic compute engine, allowing firms to choose how fast they want results by selecting how many processors to use. Beacon’s comprehensive cloud dashboard provides clear performance and capacity information, enabling customers to easily manage and monitor running and scheduled workloads.

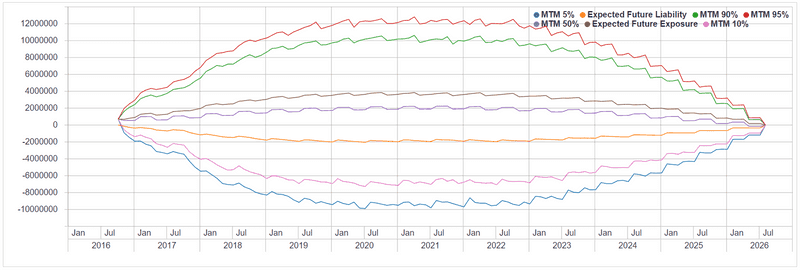

Figure 1: Expected Future Exposure (EFE) Profile and the Expected Future Liability (EFL) Profile

Leveraging the power of the platform

Beacon’s XVA Report can be run in several different modes, providing:

- Detailed profiles of Expected Future Exposure (EFE) and Potential Future Exposure (PFE) between today and the end of the longest-dated trade

- Maximum values of EFE and PFE and the future dates at which they occur

- Detailed profiles of liabilities (DVA, MEFL, MPFL)

- Detailed view of XVA statistics for a single counterparty

- Summary over multiple counterparties at once

- Intra-day Incremental “what-if” analysis XVA for new pre-trades or actual trades

- Full analysis on the Exposures and Liabilities for an arbitrary portfolio

XVA calculations in the platform use Beacon’s dependency graph, reducing the compute time and resources required. Dependency graphs are powerful tools for managing complicated chains of calculations. By automatically marking values as needing recalculation when inputs in the chain beneath them move and caching them when their inputs don’t move, our platform dramatically reduces the time for risk calculations, often by orders of magnitude.

These graphs also make it easier to understand calculation flows, analyze dependencies, and drill into calculation problems. An integrated dependency graph browser makes development and debugging of models faster and easier than other systems. Beacon’s XVA implementation also makes good use of the platform’s Financial Object Hierarchy. This simple but powerful definition of financial transactions, their dependencies, and lifecycle events makes it quick work to add or modify new financial instruments, understand and refine their pricing valuations, and include them in portfolios and risk analyses.

Enhancing platform capabilities

Beacon has recently enhanced components of the platform that are relevant to XVA calculation and reporting.

Automation & Elastic Compute: Due to their size and complexity, the ability to automate and schedule XVA calculations is an essential feature. Beacon’s job scheduling tools allow XVA reports to be set up for the necessary end-of-day and other periodic reports, typically during a quiet and lower-cost cloud computing time. Beacon can scale to 1000s of cores and use cost optimization techniques like spot instances which can reduce your compute costs by up to 90% (https://aws.amazon.com/ec2/spot/). By running the reports overnight, calculations can be quickly adjusted throughout the day for minor portfolio changes, recalculating only those paths affected by the changes. With Beacon’s elastic compute capabilities, customers can easily assign the desired number of processors for the calculation based on how quickly they need results.

Flexible Reporting: Beacon’s Trade Blotter 2.0 application provides risk professionals with reports on an existing book or portfolio, a selected set of trades, or potential pre-trades. Combined with the instrument lifecycle definitions in the Financial Object Hierarchy, these tools deliver risk assessments for a wide range of different combinations of current what-if commodity business, from the perspective of a selected counterparty. Beacon’s Trade Ingestion Framework and Trade Reconciliation Dashboard keep the portfolio of commodity trades accurate and current with intraday bookings from internal or external sources.

Driving insight and risk awareness

Beacon’s cloud infrastructure and comprehensive approach to XVA reporting eliminate the need to approximate commodity risk exposure with valuation shortcuts. Clients enjoy detailed end-of-day risk reports that facilitate faster recalculation for intra-day and pre-trade risk valuations. Traders benefit from a broader understanding of credit, debt, and liquidity risks and the lifecycle implications to the bank’s capital requirements. And risk managers have a platform that enables them to adapt and respond to evolving internal, accounting, and regulatory risk reporting requirements.